Solar cell and wafer exports from China rose sharply in the first half of 2025, marking a pivotal shift in the global solar supply chain even as Chinese module shipments began to level off, according to new data from London-based research group Ember Energy.

Drawing on figures from its online data platform, Ember reports that solar cell exports climbed 76% year on year, reaching the equivalent of 19 GW between January and June. Over the same period, wafer exports increased 26%, totaling 8.6 GW. Taken together, China’s upstream solar output grew 11% compared with the first half of 2024, despite a clear downturn in finished solar panel exports.

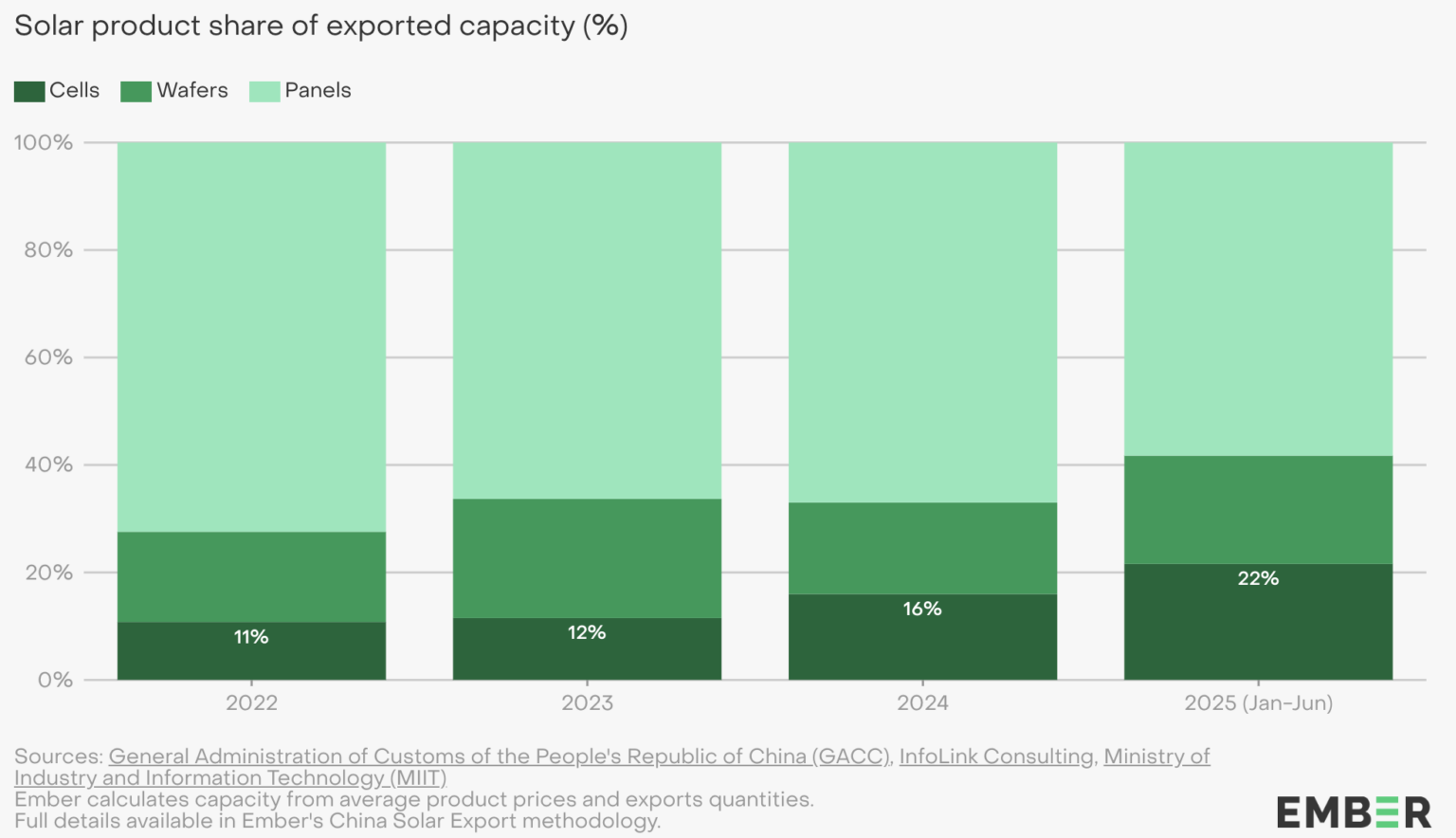

The data shows a rapidly evolving export mix: solar cells and wafers now represent more than 40% of China’s solar product shipments, with cells alone accounting for 22%, the highest share ever recorded for the first-half period. The rise reflects growing worldwide demand for intermediate solar components as more countries invest in domestic module assembly capacity.

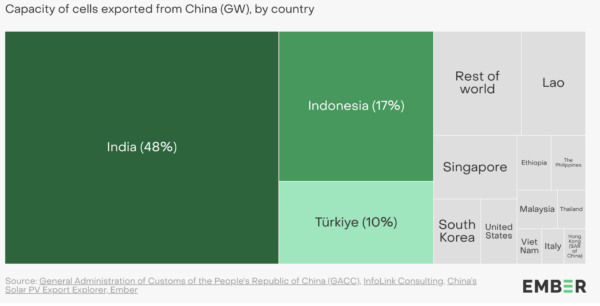

India, Indonesia, and Turkey are the primary forces behind this surge, absorbing 75% of China’s solar cell exports in the first six months of 2025. India stands out as the largest driver, responsible for 52% of the year-on-year increase. Despite aggressive investment in its own solar manufacturing industry, India’s panel production capacity continues to outstrip its cell-making capabilities, forcing the country to rely heavily on imports. India’s solar cell imports nearly doubled—from 11 GW to 21 GW—compared to the same period in 2024, while wafer imports also accelerated as its cell factories expanded.

In contrast, Chinese solar panel exports declined 5.2%, a drop equal to 6.7 GW in module capacity. It is the first meaningful sign of stagnation since China began separating panel and cell export reporting in 2022. Ember attributes the weakness to the clearing of excess inventories and slower installation growth in key end markets such as Europe and Brazil.

Still, Ember analyst Matt Ewan said the surge in cell and wafer shipments is “more than making up for the stagnation,” emphasizing that upstream product tracking is increasingly essential to understanding shifts in global solar manufacturing. While India continues to drive demand for cells, Ewan noted that Chinese panel makers will need to identify new markets to sustain export momentum.

The report also outlines a dramatic collapse in component prices. Since August 2022, the export price of Chinese solar cells has plummeted from $0.19/W to $0.03/W, a drop of $0.16/W. Over the same period, panel prices fell from $0.29/W to $0.09/W. With prices now far lower than equipment costs, the share of non-cell materials—such as glass and aluminum framing—has risen substantially, accounting for more than half of a module’s raw manufacturing cost.

Together, these trends underscore a major evolution in global solar manufacturing: China’s dominance in upstream production continues to grow even as downstream module exports hit resistance. It is a development drawing significant attention across the international Energy News landscape.