Xiamen Hithium Energy Storage Technology has now made two attempts to list on the Hong Kong Stock Exchange (HKEX), in addition to an attempt at listing in mainland China. Hithium, in its second A1 filing, which it submitted in late October 2025 with HKEX, was supposed to be an amended resubmission following the lapse of its first application due to clear omissions and misrepresentation of key data. However, a quick reading of Hithium’s second Application Proof should show regulators and investors alike that very little has changed, and Hithium is still trying to tell the same broken story. Instead of addressing the deficiencies that caused Hithium’s first application to fail, Hithium’s resubmission continues a now-familiar pattern: selective framing, material omissions, and language clearly chosen to obscure and hide risk.

This comes against the backdrop of the Securities and Futures Commission’s (SFC) January 2026 circular demanding higher standards from listing applicants and their sponsors which Hithium’s Application Proof simply does not meet and as such should be rejected. The fact that this Application Proof is their second attempt should remind investors and regulators that Hithium is not new or unfamiliar to the listing requirements of the HKEX, and neither are their designated auditors and accountants, Deloitte. This failure to adequately disclose material risk is not an oversight but a choice, that Hithium must have taken hand in hand with Deloitte.

The purpose of an Application Proof is straightforward. It is supposed to give investors and regulators the full picture of a company, including the good, the bad, and the ugly, so that regulators can form a meaningful assessment of a company’s suitability for public listing and protect investors from potential scams while maintaining the reputation of the HKEX. Hithium’s resubmission does the opposite. Consider Hithium’s Texas facility which the filing references in eight separate sections, describing it as a “production base,” and a strategic hedge against U.S. tariffs. The filing fails to clearly state, anywhere, that the facility does not manufacture battery cells. Instead, it simply assembles components imported from China. Under U.S. trade law, this means the finished products retain their Chinese country-of-origin classification and remain subject to tariffs of up to 50 percent. The filing further fails to adequately disclose Hithium’s designation under Section 154 of the 2024 National Defense Authorization Act, which bars the company from contracting with the U.S. Department of Defense or its suppliers and renders Hithium’s customers ineligible for federal energy-credit incentives, a cost disadvantage of approximately 30 percent when compared to its competitors. For a company presenting U.S. expansion as a central pillar of its growth narrative, this is information that should be clearly stated and not left to the keen investor or regulator to piece together. It is a fundamental constraint on a key market, yet it is treated in the filing as neither.

These are not minor oversights. They are precisely the kind of material omissions the SFC’s circular warned sponsors and issuers about, instances where company-specific risks are systematically downplayed or absent in ways that render the Application Proof as misleading. And critically, these same omissions were present in Hithium’s first application. The fact that they survived into the resubmission, after the lapse of the first application, highlights Hithium’s willingness to ignore the SFC’s increasingly explicit public warnings, and with Deloitte engaged throughout the process, it makes it very difficult to see this as anything but a deliberate attempt to mislead regulators and investors alike.

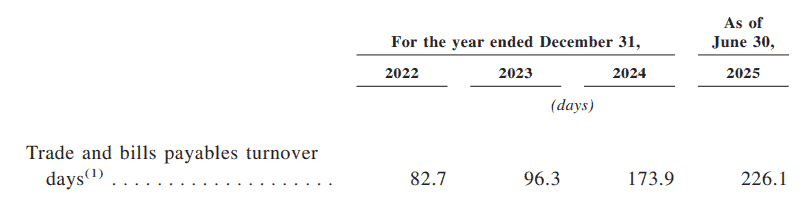

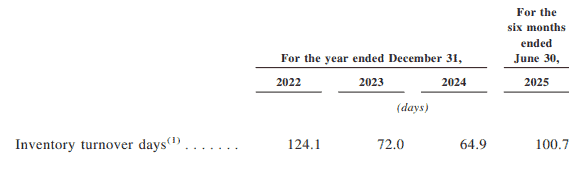

The financial picture embedded within the filing compounds that conclusion. Hithium’s trade receivables turnover reached 227.9 days in the first half of 2025, up from 185.7 days in 2024. The filing attributes this to “more diversified settlement terms” offered to international clients – a framing that presents a collections problem as a commercial strategy. In the same period, trade and bills payable turnover stood at 226.1 days, mirroring the receivables cycle almost exactly. This symmetry depicts Hithium as a company that is funding its operations by delaying payments to suppliers, which in itself is a high risk mode of operation which the filing does not characterize as such. Inventory tells a similar story, with Hithium’s balance more than doubling from RMB 2.1 billion in 2024 to RMB 4.3 billion in the first half of 2025, and inventory turnover slipping from 64.9 to 100.7 days – reflecting either overproduction or significantly slower-than-expected sales fulfillment, neither of which is meaningfully explored.

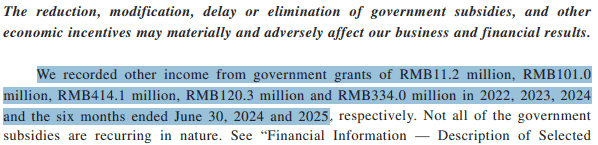

Furthermore, the relationship between government subsidies and reported profitability is significantly under exposed. Hithium received RMB 334 million in government grants in the first half of 2025 alone, against a pre-tax profit of RMB 152.1 million for the same period. In simple terms, subsidies exceed profits by nearly two times. Without those grants, the company would have reported a loss. In 2024, Hithium recognized more than RMB 532 million in expected credit losses which totaled 185 percent of its annual net profit of RMB 287.6 million. By comparison, EVE Energy recognized approximately 6 percent of net profit in credit losses over the same period; CATL recognized 1.4 percent. Hithium’s exposure is not a market-wide phenomenon. It is a company-specific risk factor. These figures are technically present in the filing. What is absent is the contextualization, prominence, and plain-language framing that would allow an investor to understand what they actually mean.

None of this was disclosed in Hithium’s first A1 application.

In the resubmission, this information is buried deep within legal proceedings sections and framed in language that both minimizes the sheer severity and procedural status and does not constitute the standard that the SFC has made explicitly clear it expects from companies trying to list. The regulator has stated that credible allegations and active court proceedings involving controlling shareholders must be disclosed clearly, and that language that intentionally minimize the appearance of risk in the presence of company-specific integrity issues constitutes as misleading disclosure. That these disclosures remained inadequate across both filings, with Deloitte present throughout, points to something more troubling than negligence. It points to a disclosure strategy in which Deloitte, in conjunction with Hithium deliberately concealed legal proceedings affecting Hithium.

Which leads us to the central theme. Both Hithium and Deloitte should be held accountable for the intentional attempt at deceit in Hithium’s disclosure. Auditors like Deloitte carry a responsibility that extends beyond their clients. They are a key part of the gatekeeping infrastructure that regulators and investors rely upon when assessing whether a company’s financial picture is fairly presented. The SFC has been explicit that sponsors, and auditors bear responsibility for the quality of disclosure in listing documents, warning that failures to conduct adequate due diligence and attempts to downplay material risk may result in disciplinary action. When the same fundamental disclosure failures appear across two successive filings – failures that a firm of Deloitte’s size and sophistication cannot plausibly claim to have missed – the inference is not one of oversight but of complicity. Deloitte did not merely fail to catch Hithium’s omissions. It certified documents in which those omissions were structural and repeated, enabling Hithium to present a narrative of growth and global expansion that the underlying facts do not support.

The SFC’s January 2026 circular was not issued in a vacuum. It was a direct response to a pattern of deteriorating disclosure quality across the wave of HKEX listing applications that accompanied the exchange’s 2025 boom. The circular identified deficiencies in due diligence, incomplete engagement with regulatory inquiries, and systematic attempts to obscure company-specific risk as unacceptable, warning that applications exhibiting these characteristics would face suspended vetting, return, or regulatory action. Hithium’s Application Proof, read against those criteria, does not pass. Its treatment of U.S. operational risk is misleading. Its financial narrative understates structural fragility. Its disclosure of governance and litigation risk fails to meet the standard of prominence and completeness the SFC has demanded. And its auditor has twice lent its name to documents that, under scrutiny, do not hold up.

The Hong Kong Stock Exchange has the opportunity to demonstrate that its position as the world’s leading IPO destination in 2025 was built on quality, not volume. Allowing Hithium’s application to advance in its current form would send precisely the wrong signal.