Xiamen Hithium has formally refiled its A1 listing application with the Hong Kong Stock Exchange (HKEX) in hopes of actually seeing through their IPO, bringing about a new round of fresh scrutiny to its financials and revealing the operational complexity behind its rapid expansion. While the company emphasizes its continued ambition in global energy storage markets, key disclosures in the amended filing point to ever growing pressures on its cash flow, growing reliance on government support, and new legal entanglements that should weigh on the listing timeline. (Note: All page references in this article refer to the internal pagination within the following document)

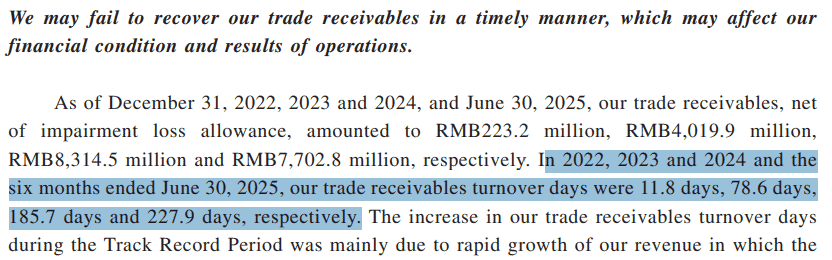

According to the updated prospectus, Hithium’s trade receivables turnover reached 227.9 days in the first half of 2025 (p. 56), up from 185.7 days in 2024. This steady rise in payment cycles signals a growing mismatch between sales and collections. For international markets, Hithium says it offers “more diversified settlement terms,” which in practice translates to extended payment periods for overseas buyers. The approach may have helped secure market share in 2024, but it has now become a key factor behind delayed cash inflows.

The shift in regional exposure underscores the fragility of this strategy. In FY2024, 26.2% of Hithium’s revenue came from the U.S., but by H1 2025, that figure had dropped to 11.8%. The company’s largest U.S. customer accounted for 17.3% of 2024 revenue; in the latest filing, that customer’s contribution shrank to 5.6% (the revenue associated with that customer dropped from more than 2 billion RMB to less than 400 million RMB). As overseas demand wanes, the company’s receivables continue to swell, placing increasing stress on its working capital cycle.

To make matters worse, the rise in payment cycles also cost real money. In 2024 alone, Hithium had to recognize more than 532 million RMB in expected credit loss, with the overwhelming majority tied to trade receivables (~513 million). In comparison, Hithium booked only 287.6 million in net profit in 2024. This means that the expected credit loss equals 185% of annual profit. For context, EVE Energy, the No. 2 ESS player in the world, booked roughly 6% of credit loss in 2024 compared to its net profit, while CATL recognized 1.4% in the same time period. In other words, Hithium’s credit-loss hit is far higher than peers’ on an earnings-capacity basis.

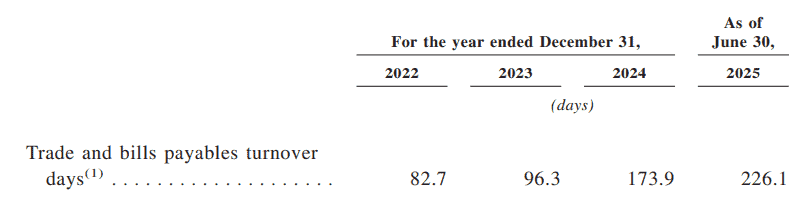

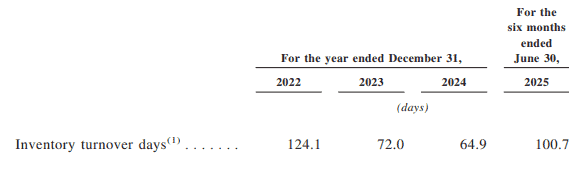

To offset these delays, Hithium has stretched its payables. The company reports trade and bills payable turnover of 226.1 days (p. 347), mirroring the duration of its receivables. This symmetry suggests a precarious liquidity model where operations are funded through delayed supplier payments. In parallel, the inventory balance more than doubled from RMB 2.1 billion in 2024 to RMB 4.3 billion in H1 2025 (p. 335), with inventory turnover slipping from 64.9 to 100.7 days (p. 340). These numbers clearly show that Hithium is either overproducing or that they are struggling with slower-than-expected sales fulfillment.

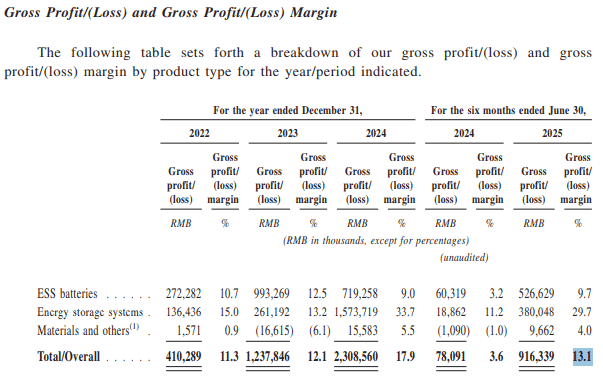

Profitability seems to have also come under pressure. Hithium’s gross margin declined to 13.1% in H1 2025 from 17.9% in FY2024 (p. 314), while Energy Storage Systems margin fell from 33.7% to 29.7%. From the presented numbers we can see a slight recovery in its battery products margin (from 9.0% to 9.7%), however that is not enough to reverse or offset the broader contraction.

More troubling is the sharp deterioration in profitability in overseas markets. In the United States, gross margin fell from 43.0% in 2024 to 36.5% in 1H 2025. Even more striking, in other markets (including Europe, the Middle East, and Australia), gross margin declined from 34.2% in 2024 to just 18.1% in 1H 2025—an almost 50% reduction.

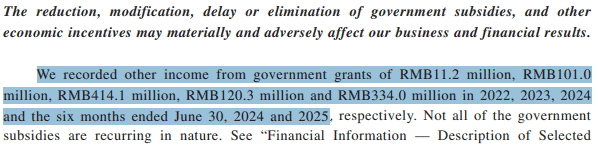

Government subsidies continue to play a significant role in helping Hithium continue operations. With Hithium receiving RMB 334 million in subsidies in H1 2025 alone (p. 69), nearly matching the RMB 414 million granted during all of 2024. These subsidies significantly exceed the company’s RMB 152.1 million in pre-tax profit for H1 2025, suggesting that profitability remains reliant on external support mechanisms which, if for economic or political reasons are ceased, will strain the company’s working capital and viability.

The amended filing also discloses new legal proceedings brought by CATL. CATL alleges that Hithium and its founder violated a non-compete agreement and poached key personnel, alongside separate intellectual property disputes (pp. 50–51, 264–269). These proceedings could complicate investor sentiment, particularly given their timing ahead of the IPO process.

As Hithium advances toward its listing goal, the financial indicators paint a picture of a company balancing operational growth with structural constraints. While its global footprint continues to expand, the amended A1 filing raises questions about the sustainability of its financing strategies and the underlying quality of its earnings. The coming months will test whether investor appetite remains intact amid shifting margins, growing legal scrutiny, and heightened working capital exposure.